- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Summary

QLV is designed to help investors manage equity risk without stepping away from the market.

By combining low volatility with a quality screen, the strategy targets companies with more stable price behavior and stronger fundamentals.

The result is a resilient approach to U.S. equities that aims to reduce portfolio swings while remaining invested through market cycles.

What is QLV and why was it created?

QLV is designed for investors who want to stay engaged in equity markets with greater confidence – seeking resilient equity exposure that participates in market upside while providing a stabilizing influence during periods of market stress. It was created to address the limitations of traditional low volatility strategies, which can unintentionally concentrate portfolios in specific sectors or introduce interest‑rate sensitivity.

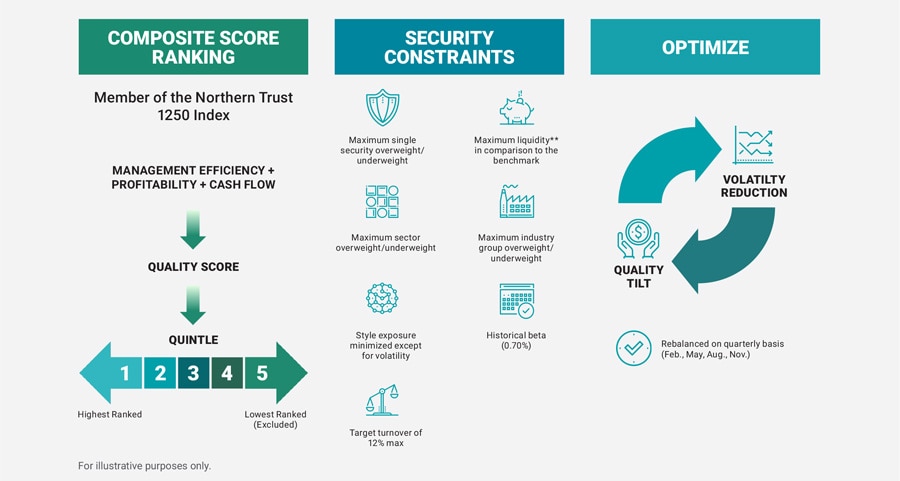

QLV tracks the Northern Trust Quality Low Volatility Index, which selects U.S. large‑ and mid‑cap companies that exhibit lower overall volatility while also meeting quality criteria related to profitability, management efficiency, and cash flow.

How does QLV differ from traditional low volatility ETFs?

Many low volatility strategies focus narrowly on past price movements, which can lead to heavy exposure to sectors that appear stable but carry other risks. QLV takes a broader view by providing balanced exposure across sectors and integrating quality into the security selection process.

By emphasizing financially stronger companies alongside lower volatility, QLV seeks to avoid some of the unintended sector and factor concentrations that can emerge in purely volatility‑based approaches.

Why does quality matter in a low volatility strategy?

Research suggests that lower‑quality companies have historically exhibited higher volatility, particularly during periods of market stress. Quality metrics such as profitability, management efficiency, and cash flow can help distinguish between companies that are merely stable in price and those that are fundamentally resilient.

Past volatility is not always predictive of future volatility. QLV integrates quality to provide a forward‑looking complement to volatility, helping reduce reliance on backward‑looking price behavior alone.

How does QLV manage sector and security concentration risk?

QLV applies explicit diversification and risk controls during index construction, including limits on individual securities, industries, and sectors. These constraints are designed to prevent the portfolio from becoming overly concentrated in traditionally defensive sectors. These sectors, such as utilities and consumer staples, carry a lot of macroeconomic risk—especially exposure to interest rates.

The strategy also targets a lower overall market beta while maintaining broad exposure across the U.S. equity market, helping balance risk reduction with diversification.

Is QLV meant to be used tactically or strategically?

QLV is designed as a strategic defensive position in an investors equity portfolio. Volatility events and drawdowns are highly unpredictable, and it is important to already be invested in the strategy when they occur. The differentiator for QLV to other low volatility strategies is that it is not designed to only provide benefits during drawdowns. Markets go up more than they go down, and we’ve designed QLV to be held strategically throughout the market cycle.

What types of market environments is QLV designed for?

QLV is built to navigate a range of market environments, particularly those marked by uncertainty or elevated volatility. The strategy aims to dampen drawdowns during market stress while still participating in equity upside when markets recover.

Its design reflects a focus on consistency rather than maximizing returns in any single market regime.

How should advisors think about QLV relative to other low volatility strategies?

QLV takes a more balanced approach than traditional low volatility strategies. Low volatility strategies often overemphasize risk reduction, which can result in significant deviations from the broader market and reduced upside participation. By pairing volatility reduction with quality considerations, QLV is designed to function as a core equity holding rather than a narrow risk‑hedging tool.

Where does QLV typically fit in a portfolio?

QLV is commonly used as a core U.S. equity allocation for investors seeking to manage risk without sacrificing equity exposure. It may also serve as a complement to more growth‑oriented strategies, helping smooth overall portfolio volatility.

Advisors may pair QLV with international equities, income strategies, or satellite allocations to build a more balanced portfolio.

Contact Us

Interested in learning more about our expertise and how we can help?

IMPORTANT INFORMATION

Before investing, carefully consider the FlexShares investment objectives, risks, charges and expenses. This and other information is in the prospectus, a copy of which may be obtained by visiting www.flexshares.com. Read the prospectus carefully before you invest.

Foreside Fund Service, LLC, distributor. FlexShares and Foreside are not related.

FlexShares Credit -Scored US Corporate Bond Index Fund (SKOR) is passively managed and uses a representative sampling strategy to track its underlying index. Use of a representative sampling strategy creates Tracking Risk where the Fund’s performance could vary substantially from the performance of the underlying index along with the risk of high portfolio turnover.

As with any investment, you could lose all or part of your investment in a FlexShares ETF, and the ETF’s performance could trail that of other investments. An ETF is subject to certain risks, including the principal risks notes below, any of which may adversely affect the ETF’s net asset value (“NAV”), trading price, yield, total return and ability to meet its investment objective.

For more complete information on the Fund’s Principal Risks, please read the prospectus and summary prospectus, including all principal risk information such as: Concentration Risk (Financial Sector), Income Risk, Credit (or Default) Risk, Interest/Maturity Risk and other principal risks. Copies of the prospectus and summary prospectus may be obtained by visiting www.flexshares.com. Read the prospectus carefully before you invest.

Corporate Bond Risk is the risk the Fund faces because it invests primarily in bonds issued by corporations. Quality-Value Score Risk is the risk that the Fund’s investment in companies whose securities are believed to be undervalued will not appreciate in value as anticipated or the past performance of companies that have exhibited quality characteristics does not continue. Authorized Participant Concentration Risk is the risk that the Fund may be adversely affected because it has a limited number of institutions that act as authorized participants. Market Trading Risk is the risk that the Fund faces because its shares are listed on a securities exchange, including the potential lack of an active market for Fund shares, losses from trading in secondary markets, periods of high volatility and disruption in the creation/redemption process of the Fund. ANY OF THESE FACTORS MAY LEAD TO THE FUND’S SHARES TRADING AT A PREMIUM OR DISCOUNT TO NAV.

© 2026 Northern Trust Corporation. Head Office: 50 South La Salle Street, Chicago, Illinois 60603 U.S.A.