- Who We Serve

- What We Do

- About Us

- Insights & Research

- Who We Serve

- What We Do

- About Us

- Insights & Research

Streamlining Bond Ladder Management with Distributing Ladder ETFs

Learn how Northern Trust Distributing Ladder ETFs help financial advisors manage cash flow more efficiently by simplifying bond ladder construction, streamlining implementation, and scaling access consistently across client portfolios.

Key Points

What it is

Distributing Ladder ETFs package professionally built bond ladders into a single, scalable position that helps to reduce operational friction.

Why it matters

They seek to deliver predictable monthly income and scheduled principal return while aiming to preserve core ladder benefits like staggered maturities and duration control.

Where it's going

Advisors and their teams gain time, cleaner statements, and simpler workflows.

Question: What are Distributing Ladder ETFs and why did NTAM build them?

Answer: Distributing Ladder ETFs are designed to provide a single, tradeable position representing a professionally built ladder across defined maturities. Advisors wanted to keep the logic of ladders while removing the day‑to‑day process work that slows teams down.

These ETFs aim to do exactly that. They are designed to preserve the ladder’s rungs and transparent maturity path but simplify execution and reporting. For practices managing many accounts and timelines, one ETF instead of many bonds means fewer tickets, fewer system touches, and a consistent process for cash flow management. The goal: retain benefits, reduce burden.

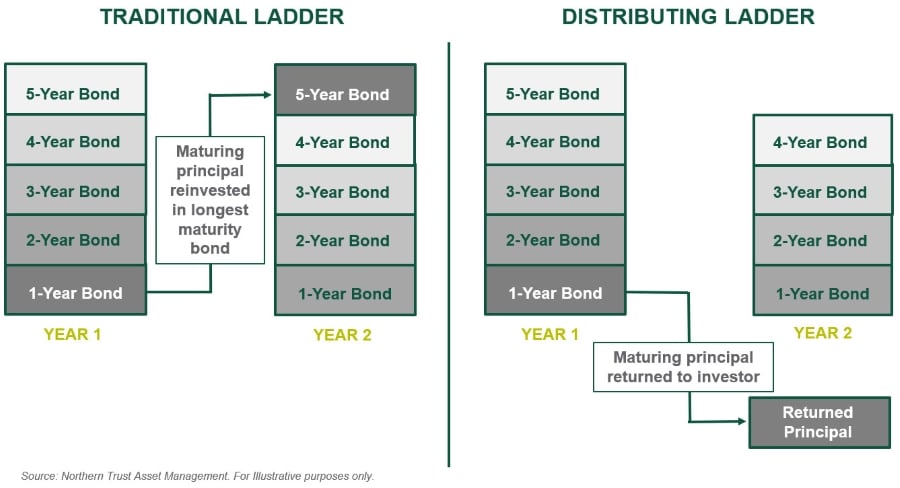

Traditional Bond Ladders vs. Distributing Ladders

While traditional bond ladders are built for manual reinvestment as each bond matures, distributing ladder EFTs distribute the principle from maturing bonds annually to provide consistent cash flow.

Q: How do Distributing Ladder ETFs change the operational workload for advisors and their teams?

A: The change is immediate. Instead of building ten or more positions per client, a team trades one ETF and tracks one line item on statements. That means less time with trading desks and fewer steps in workflows.

Reviews are faster because the story is clear: monthly income shows in one position, principal return follows an annual schedule, and the maturity profile is easy to explain. Teams use saved time for client conversations and proposals rather than stitching together bond details. In short, the ETF reduces work while keeping the plan intact.

Q: Do Distributing Ladder ETFs preserve the core benefits of traditional ladders?

A: Yes. The structure that makes ladders valuable remains. Staggered maturities help manage interest rate exposure and duration, so advisors can map time to client dates confidently. Transparency into holdings and the maturity path supports clear planning conversations. Scheduled principal return aligns to spending needs without adding complexity. These are why ladders work. Distributing Ladder ETFs keep those benefits while giving advisors a cleaner way to implement across books of business without sacrificing outcomes.

Q: How does this scale across a book with different time horizons?

A: Variety is the norm. One client may need a 10‑year ladder, another 15 or 20 years, and the weighted average across the book may sit near 12.5 years. The Distributing Ladder approach scales because each client’s investment lives as one ETF position. Advisors can tailor size and horizon at the account level, yet the operational footprint stays simple. Now, executing this investment strategy across multiple client portfolios no longer multiplies bond sourcing, trade tickets, and reconciliations. It is as straightforward as onboarding a new position, documenting the cash flow timeline, and dropping the ETF into your planning cadence and model framework.

Q: What is the practical impact on client experience and review meetings?

A: Clients see clarity. One position replaces a cluster of bonds, so statements are clean and conversations focus on goals and cash flow rather than coupons and cusips. Advisors can show a simple timeline for monthly income and annual principal distributions that align to cash flow needs. This keeps meetings efficient and reduces follow‑up confusion. For teams handling many reviews each quarter, consistency matters. It saves time, may improve recommendations, and helps clients leave with a clear understanding of how Distributing Ladders support their plan.

Q: Where do municipal ladders fit, given credit selection and execution realities?

A: Muni ladders benefit the most from expert selection. Northern Trust Tax-Exempt Distributing Ladder ETFs leverage a professional team of municipal investors that provide issuer screening, sizing, call features, and credit oversight. Advisors avoid odd lots and partial fills that clutter statements and consume time. The result is federal tax‑free cash flow that appears as a single line item, with transparent visibility into the principal schedule. It improves execution quality and reduces operational risk. For practices serving many muni clients, consolidating selection and reporting into one position lifts service quality without expanding internal processes.

Q: How do Distributing Ladder ETFs fit alongside existing models?

A: Integration is straightforward. Distributing Ladder ETFs fit into tax‑exempt, inflation‑linked, or blended sleeves and treat time as a deliberate portfolio input. Advisors can align maturities to goal dates, size allocations within model constraints, and track progress with standardized reports. Because the ladder is an ETF, operations and compliance teams see consistent documentation and lower variance across reviews. For larger firms, fewer system steps and cleaner audit trails maintain momentum. The result: a planning tool that supports disciplined outcomes while freeing capacity for client engagement and growth.

Q: What’s next? Will Northern Trust launch additional ladder suites or other solutions?

A: Northern Trust Asset Management remains focused on enhancing outcomes and simplifying processes for advisors. Our commitment is to deliver products, whether ladders or other structures, that meet these ambitions.

Northern Trust Tax-Exempt Distributing Ladder ETFs | Northern Trust Inflation-Linked Distributing Ladder ETFs |

|---|---|

MUNA 5 years (2030)

|

TIPA 5 years (2030)

|

Low Fees: 18 BPS** | Low Fees: 10 BPS** |

*Individual bonds carry an obligation to fully return principal to investors at maturity, however ETFs have no such obligation. The net asset value of the ETFs will decline over time as income payments are made to shareholders.

**18 basis points (BPS, or 0.18%) and 10 basis points (BPS, 0.10%) refers to both net and gross expense ratios. Interest on municipals is exempt from federal income tax but may be subject to state and local tax. This information is general in nature and should not be construed as tax advice.

Related Content

Contact Us

Interested in learning more about our expertise and how we can help?

IMPORTANT INFORMATION

Before investing, carefully consider the investment objectives, risks, charges, and expenses. This and other information is in the prospectus and a summary prospectus, copies of which may be obtained by visiting www.flexshares.com or calling 855-353-9383. Read the prospectus carefully before you invest. Northern Funds Distributors, LLC, distributor. Northern Funds Distributors, LLC and FlexShares are not affiliated with Northern Trust.

All investments are subject to investment risk, including the possible loss of principal amount invested. Investments do not typically grow at an even rate of return and may experience negative growth. As with any type of portfolio structuring, attempting to reduce risk and increase return could, at certain times, unintentionally reduce returns.

Individual bonds carry an obligation to fully return principal to investors at maturity, however ETFs have no such obligation. The net asset value of the ETFs will decline over time as income payments are made to shareholders.

Not FDIC insured | May lose value | No bank guarantee

As with any fund, it is possible to lose money on an investment in the Fund. An investment in the Fund is not a deposit of any bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation, any other government agency, or The Northern Trust Company, its affiliates, subsidiaries or any other bank.

ETFs are subject to additional risks that do not apply to conventional mutual funds, including the risks that the market price of an ETF’s shares may trade at a premium or discount to its net asset value, an active secondary trading market may not develop or be maintained, or trading may be halted by the exchange in which they trade, which may impact an ETF’s ability to sell its shares. Shares of any ETF are bought and sold at market price (not NAV) and are not individually redeemed from the ETF. Brokerage commissions will reduce returns.

RISKS APPLICABLE TO BOTH TAX-EXEMPT AND INFLATION-LINKED DISTRIBUTING LADDER ETFs

{{credit_risk}}

Fluctuation of Yield and Principal Payment Risk is the risk that the Fund, unlike a direct investment in a bond that has a level coupon payment and a fixed payment at maturity, will make distributions of income that vary over time. Unlike a direct investment in bonds, the breakdown of returns between Fund distributions are not predictable at the time of your investment.

Fund Termination Risk is the risk that, unlike an investment in a traditional investment company with perpetual existence, the Fund is designed to liquidate in the terminal year and thus a shareholder of the Fund will not receive distributions from the Fund beyond the terminal year.

{{liquidity_risk}}

{{non_diversification_risk}}

Return of Capital/Distribution Risk is the risk that the Fund’s distributions will involve a return of capital, which, although not currently taxable, may lower a shareholder’s basis in the Fund’s shares, thus potentially subjecting the shareholder to future tax consequences in connection with the sale of Fund shares, even if sold at a loss to the shareholder’s original investment.

Small Fund Risk is the risk that the Fund will not grow to or maintain an economically viable size, in which case it may liquidate prior to the anticipated liquidation date in the terminal year, thus impacting the Fund’s ability to achieve its investment objective.

RISKS APPLICABLE TO NORTHERN TRUST TAX-EXEMPT DISTRIBUTING LADDER ETFS

Municipal Investments Risk is the risk that the value of a municipal security generally depends on the financial and credit status of the issuer. Constitutional amendments, legislative enactments, executive orders, administrative regulations, voter initiatives, and the issuer’s regional economic conditions may affect a municipal security’s value, interest payments, repayment of principal and the Fund’s ability to sell the security.

Municipal Market Volatility Risk is the risk that the Fund may be adversely affected by volatility in the municipal market. The municipal market can be significantly affected by adverse tax, legislative, political or public health changes and the financial condition of the issuers of municipal securities.

Municipal Tax Liability Risk is the risk that shareholders of the Fund could be subject to tax liabilities. The Fund will invest in municipal securities in reliance at the time of purchase on an opinion of bond counsel to the issuer that the interest paid on those securities will be excludable from gross income for regular federal income tax purposes.

RISKS APPLICABLE TO NORTHERN TRUST INFLATION-LINKED DISTRIBUTING LADDER ETFS

Inflation-Indexed Securities Risk is the risk that the value of inflation protected securities, such as TIPS, generally will fluctuate in response to changes in real interest rates, generally decreasing when real interest rates rise and increasing when real interest rates fall. In addition, interest payments on inflation-protected securities will generally vary up or down along with the rate of inflation.